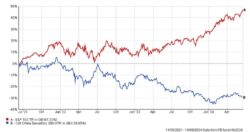

After a decade of rapid growth, China has offered scant reward for investors since 2021. Where developed western markets have enjoyed strong returns since November, Chinese Equities continue to forge a contrarian path lower, despite a growing number of reasons why China appears to offer good value to investors. The graph below demonstrates the very different performance of the CSI China 300 index (shown in blue) compared to the S&P500 index of leading US companies (shown in red), priced in Sterling, over the last 3 years.

We take a look at some of the factors that have led to the underperformance, and outline reasons why we feel an allocation to China deserves a place in a diversified portfolio.

The Chinese economy has traditionally expanded at a rapid pace, with annualised growth of between 6% and 10% per annum achieved between 2010 and 20191; however, the rate of growth on an annualised basis has slowed over recent years. Covid-19 caused Gross Domestic Product (GDP) growth to dip, as was the case across the World, although the Chinese economy rebounded last year, growing by 5.24%. This rate of growth compares favourably to the US, which itself expanded by an impressive 3.1%, and very appealing when you consider the meagre growth achieved by the UK and Eurozone last year. Although the rate of growth predicted for the Chinese economy over the next five years is lower than pre-Covid levels, economists predict an annualised growth rate of around 4% per annum, which may well look attractive when compared to other leading economies.

The Covid-19 pandemic was particularly damaging to the Chinese economy. Harsh lockdown rules capped economic activity to a large extent, and when the restrictions were eased in November 2022, economists expected a rapid acceleration and recovery, as domestic consumption rebounded and consumers spent money saved during the pandemic.

The reality has been very different to expectations, as consumer confidence remained stubbornly weak post-pandemic. Very recent data has, however, indicated a slight improvement, with retail sales for May growing by 3.7% year on year2, reversing the downward trend seen over recent months.

Most western economies struggled to contain spiralling inflation during 2022 and 2023, caused by increased demand for goods and services post pandemic, and the impact of war between Russia and Ukraine, which pushed commodity prices higher. Given the sluggish recovery in consumer confidence seen in China, inflation was barely positive for 2023, and the International Monetary Fund (IMF) predict Chinese inflation will only reach 1% this year.

Beijing has already taken measures in an attempt to stimulate demand, such as offering trade-in subsidies against the purchase of new cars and white goods, and cutting base interest rates late in 2023. It is likely, however, that further monetary stimulus will be needed, which could prove a fillip for investors.

Unemployment levels amongst young people also remains a concern, with 14.2% of those aged 16 to 24, who are not in full time education, looking for work2. That being said, this has steadily fallen from the 20% level seen last year, and we expect to see further measures to boost productivity and employment prospects, in particular in areas such as technology.

One key reason behind the underperformance of Chinese Equities since 2021 has been the continued struggles seen in the real estate sector. Land and Property development, which according to analysts accounted for almost one third of China’s GDP at one point, boomed during the last decade, with much of the growth fuelled by debt. Overdevelopment saw a glut of unsold properties, spawning ghost cities amidst a buyers strike. Lack of consumer confidence in the wake of the pandemic, and demographic shifts are often cited as the key reasons for the extended slump in real estate prices.

As demand eased, and debts mounted, pressure began to bear on the largest property enterprises. Evergrande, a key player in the Chinese property market and at one point the most valuable property company in the World, defaulted on its debt in 2021, and eventually filed for bankruptcy in August 2023. Country Garden, another leading property firm, saw its shares suspended earlier this year. The company has also defaulted on loans and is facing a liquidation petition.

Concerns over the impact that defaults could have on the strength of local and national banks remain, although the immediate prospects of a property-led banking crisis now appear less likely. China’s Government have announced a raft of measures in an attempt to arrest the decline, including the purchase of unsold homes by local authorities, although further action will almost certainly be needed to help boost confidence in the sector. Any such moves would be welcome; however, we expect the property sector to be a drag on growth for some time to come.

The increased focus on new industry, such as electric vehicles, is a good example where Chinese companies have the potential to dominate global supply. A slow but steady move towards net zero will require change on a colossal scale, and a gradual move away from traditional manufacturing to added value could halt the decline in industrial production seen over recent years.

The poor performance of Chinese Equities since 2021 has led to valuations becoming increasingly cheap when compared to other developed markets. Estimates of the forward price to earnings ratio suggest that the MSCI China Index stands at between 11 and 13 times earnings, which is roughly the same level of market valuation as the UK, despite the fact that China is likely to grow their economy at more than double the pace of the UK over the next five years.

Despite the apparent inherent value, investment in China is not without risks. Continued pressure from the ailing property sector, ongoing tensions with the West and the potential for regulatory interference temper our enthusiasm, and given the outflows seen from Chinese Equities over the past two years, investment at this point would be considered a contrarian move.

Taking all factors into consideration, we see the potential for a rebound in the fortunes of Chinese Equities over the medium term. Investors will, however, need to show patience, and volatility may well be uncomfortable at times. We therefore feel that an allocation to China could be appropriate; however it is important to hold a diversified portfolio of assets, and our experienced team can provide advice to tailor your portfolio to suit your tolerance to investment risk, whilst ensuring diversification is maintained. Speak to us to start a conversation about the asset allocation within your investment or pension portfolio.

Sources

1 World Bank Group

2 National Bureau of Statistics of China